Diesel Displacement Lab: The Drop-in Opportunity

Australia is deeply reliant on diesel, but also heavily exposed, importing over 90% of it. In this blog, I unpack the opportunity that lies with drop-in fuels for diesel displacement.

About Diesel Displacement Lab

🚛 Diesel is everywhere.

🛠️ It’s stubborn. It’s sticky.

📉 I’m on a mission to shift that.

By 2035, I’ve set a personal target:

⚡ Displace the equivalent of 1% of Australia’s diesel use.

This blog is my Diesel Displacement Lab—

🔍 A space to explore how diesel is used today

🧪 Spot tech that can actually replace it

💸 And back lab-to-market founders with my time and capital

Blog structure - read what’s important to you!

Section 1: Scene-setting on how diesel is used today in Australia

Section 2: Where does our diesel come from?

Section 3: What are drop-in fuels and why are they relevant?

Section 4: My view on where to play for drop-in fuels

Section 5: My view on where the technology opportunities are for drop-in fuels

1. Australia’s Diesel Dependence

⛽ Australia’s diesel dependence

Diesel, a distillate of crude oil, is a critical fuel for Australia’s economy, powering a wide range of activities across transport, mining, agriculture, and construction. Its high energy density and efficiency make it suitable for heavy-duty applications, including long-haul trucks, mining equipment, agricultural machinery, and construction vehicles. Given Australia’s vast geography and resource-based economy, diesel plays a pivotal role in supporting both urban and remote operations, particularly in sectors with significant energy demands.

In 2023-24, total diesel consumption in Australia reached approximately 33 billion litres, reflecting its widespread use across industries (Australian Petroleum Statistics).

🔎 How is diesel used by industry:

🚚 Transport: Consumes ~18.3 billion litres of diesel p.a. representing ~73% of the energy mix.

⛏️ Mining: Consumes ~8.1 billion litres p.a. representing 41% of the energy mix.

🌾 Agriculture: Consumes ~4.0 billion litres p.a. representing 84% of the energy mix.

🏗️ Construction: Consumes ~2.3 billion litres p.a. representing ~50% of the energy mix.

(Department of Climate Change, Energy, the Environment and Water)

🍯 Why is diesel so ‘sticky’ as a fuel type in Australia?

It’s all about its key characteristics: high energy density for long-haul stamina, storability for remote operations, and compatibility with a massive fleet of engines already in play.

Any solution aiming to rival it, needs to bring the same ‘muscle’:

💪 Enough power to move a mining truck or plow a field

🛢️ Reliable storage — sits in a tank without a fuss in any climate

🔌 Plug-and-play compatibility — no major transition cost or system overhaul

🧾 Diesel’s Cost Edge and the Excise Advantage

Following diesel’s entrenched role across Australia’s industries, its stickiness gets an extra boost from the nation’s fuel excise system, pegged at around 50 cents per litre (Australian Tax Office). The Fuel Tax Credit scheme provides a lifeline to heavy hitters like mining and agriculture, letting them recover some or all of that excise for off-road use, reducing their fuel bills. With credits tied to the Consumer Price Index, these rebates keep pace with inflation, keeping diesel’s cost edge sharp against pricier low-carbon options.

A 50-cent-per-litre excise credit on fossil diesel, which averaged $1.77 AUD per litre across Australia’s top 5 capital cities in December 2024, can effectively lower the fossil diesel cost by as much as 28%. This advantage creates an additional barrier for emerging diesel displacement solutions that do not meet the credit’s eligibility requirements (Australian Competition & Consumer Commission, Australian Tax Office).

2. Australia’s Current Diesel Supply Equation

🇦🇺⚖️🌍 Australia’s Diesel Supply Mix: Domestic vs. Import

Australia relies on imports for the vast majority of its diesel, with around 29.8 billion litres imported in the financial year 2023, compared to total consumption of about 33 billion litres, suggesting domestic production covers roughly 3.2 billion litres, or less than 10% (Statista, Australian Petroleum Statistics).

Australia’s heavy import dependence stems from insufficient local refining capacity to meet demand, with only two remaining refineries—Ampol’s Lytton in Brisbane and Viva Energy’s Geelong—producing only a fraction of what’s needed. This is a sharp decline from 2000, when there were eight refineries; by 2021, closures like BP’s Kwinana and ExxonMobil’s Altona reduced the count to two, now mainly serving as import terminals (Shipping Australia). This reduction is driven predominantly by economic factors, as Australian refineries struggled to compete with larger, more efficient Asian refineries due to cost, scale, and technology differences, so its cheaper to import refined products as opposed to refining domestically.

Australia’s heavy reliance on imported diesel poses a serious risk to energy sovereignty, given diesel’s role as the backbone of our industries!

Diesel displacement opens the door for Australia to leverage its considerable strengths in renewable energy, feedstock abundance and domestic capability to reduce reliance on imported diesel, strengthen energy resilience, and enable new economic opportunities.

3. How Can Australia Displace Fossil Fuel Based Diesel?

🔄 The Drop-in Opportunity

Drop-in fuels are renewable alternatives designed to replace conventional fossil fuels like diesel without requiring modifications to existing engines, pipelines, or storage systems. They’re called “drop-in” because they can be seamlessly integrated into current infrastructure, making them a practical solution for decarbonising heavy industries such as transportation, mining, and agriculture. For diesel, the two leading drop-in fuel candidates are biodiesel (also known as hydrotreated vegetable oil, or HVO) and renewable diesel (a chemically identical substitute for fossil diesel).

🌾 Leading Pathways for Biodiesel and Renewable Diesel

Biodiesel:

Produced through a process called transesterification, where feedstocks like vegetable oils (e.g., canola, soybean), used cooking oil, or animal fats (e.g., tallow) are reacted with an alcohol, typically methanol, and a catalyst (e.g., sodium hydroxide). This reaction converts the oils into fatty acid methyl esters (FAME), the chemical name for biodiesel, and glycerol as a byproduct. The biodiesel is then purified for use.

In Australia, Eco Tech Biodiesel collect used cooking oil from local restaurants and process it into biodiesel via transesterification at their Narangba facility in Queensland. The plant has a capacity of about 10 million litres per year, and supplies drop-in fuels for local fleets.

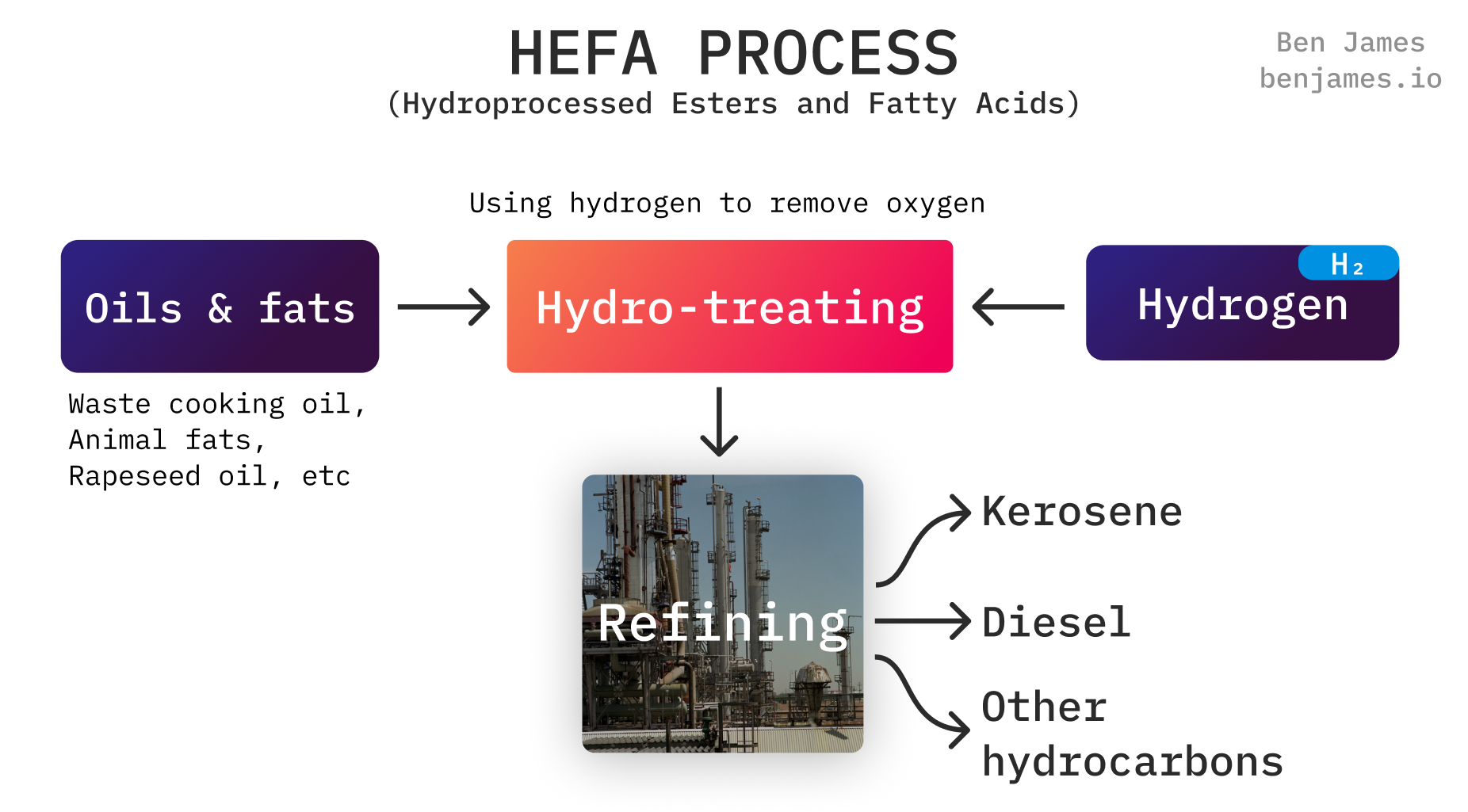

Renewable diesel:

In this blog, we’ll focus only on the biogenic pathway for producing renewable diesel through hydrotreatement, where organic feedstocks such as waste oils, tallow, or even lignocellulosic biomass are converted into renewable diesel. This pathway will be the focus as it currently, presents the most established and cost-effective option for diesel displacement.

A summary of the other emerging pathways can be found here in a blog from Ben James, which I found quite insightful! Note - renewable diesel and sustainable aviation fuel are co-products, so the content from Ben’s blog also applies to renewable diesel.

The hydrotreatment process involves the treatment of organic feedstocks with hydrogen at high temperatures and pressures, which removes the oxygen and impurities present within the to feedstock, to produce a hydrocarbon that is chemically identical to fossil diesel. Unlike biodiesel, renewable diesel contains no oxygen molecules, giving it better stability and compatibility.

A notable Australian example is Viva Energy’s trials at its Geelong Refinery. In 2023, Viva processed waste oils into renewable diesel onsite, leveraging existing hydrotreatment units to produce small batches for testing in heavy vehicles. While not yet scaled, this demonstrates the potential for refineries to pivot to drop-in fuels.

⚖️ Drop-In Fuels vs. Fossil Diesel: Characteristics, Blends, and Decarbonisation Benefit

Characteristics and Blends:

Biodiesel (FAME) has slightly different chemical properties, with oxygen content that can affect stability and cold flow, limiting blends to B5-B20 (5-20% biodiesel) in most diesel engines without modification, though higher blends like B100 are possible with adjustments.

Renewable diesel, being chemically identical to fossil diesel, can be used as a 100% replacement or in any blend ratio, offering greater flexibility.

Decarbonisation Benefit:

Biodiesel cuts emissions by 20-80%, depending on the feedstock (e.g., waste oils perform better than virgin crops), per (CSIRO’s - Low Carbon Liquid Fuel Opportunities).

Renewable diesel achieves 60-80% reductions, with waste-based HVO at the higher end. These savings stem from using renewable feedstocks that absorb carbon emissions during growth or repurpose waste, unlike fossil diesel’s extraction-heavy carbon footprint. (Transport for NSW)

🏷️ How does it stack-up on cost?

Biodiesel averages between $1.57–$2 AUD per litre, which represents a competitive displacement solution that ranges between 0.9 - 1.1x the price of fossil diesel (Biodiesel industries).

Renewable diesel production is yet to come online in Australia, however recent consultation responses to the Future Made in Australia: Unlocking Australia’s low carbon liquid fuel opportunity indicated the price could be ~1.5x the price of fossil diesel (in the best case scenario) under the biogenic pathway (Australiasian Convenience and Petroleum Marketers Association).

What drives the cost of drop-in fuels?

The economics of drop-in fuels are shaped by a few key cost drivers:

🌾 Feedstock is the #1 cost – Inputs like UCO, tallow, and camelina are scarce, globally competitive, and costly to collect in Australia.

🚛 Logistics are expensive – Fragmented supply chains and long distances drive up transport and pre-treatment costs.

🏭 Refining is capital-intensive – Hydrotreating and isomerisation need fossil infrastructure or costly greenfield builds.

⚡ Green hydrogen adds cost – A critical input for renewable diesel, but still expensive and limited in supply in the near-term.

📉 Small scale = high cost – Many plants lack scale or run below capacity due to policy or feedstock gaps, pushing per-litre costs higher.

🚧 What are the key barriers to entry for drop-in fuels?

📈 Intense competition for feedstock – Demand from food, feed, and export markets drives volatility and inflates costs.

📜 Contract vs. capital mismatch – Short-term or uncertain feedstock agreements clash with the long-term certainty financiers require.

🛢️✈️ SAF vs. renewable diesel tension – Co-produced through the same process, but producers must weigh:

💰 Higher margins for renewable diesel

🚀 Greater policy and market momentum for SAF

🏭 Refining limitations – Australia lacks scalable infrastructure for hydrotreated fuels, and upgrades face high cost and long lead times.

4. My take on where to play for drop-in fuels

Drop-in fuels won’t replace diesel everywhere, but they have the potential to play a transitionary role in Australia’s decarbonisation strategy, particularly in the next decade. Their biggest advantage? They’re ready now. Drop-in fuels work with existing engines, fuel supply chains, and distribution networks, enabling emissions reductions without waiting on new infrastructure or vehicle transitions.

They’re especially relevant in diesel-reliant sectors where alternatives are still maturing, including:

⛏️ Mining, agriculture, and long-haul freight, where engines run hard, long, and remote.

🌾 Remote and off-grid regions, where power reliability is critical and logistics are complex.

⚡ Backup generation and industrial equipment, where uptime matters more than drivetrain.

Crucially, Australia’s energy transition faces structural delays:

🔌 Transmission infrastructure, which is the backbone of electrification has multi-year lead times and significant cost and approval hurdles in regional areas.

🌥️ Renewable energy’s intermittency challenges impacts reliability for 24/7 industrial operations, especially without mature storage solutions.

These gaps mean electrification pathways will take time to reach remote diesel users. In contrast, drop-in fuels can be blended into current systems today, offering a low-disruption, near-term emissions solution.

While costs remain a barrier, drop-in fuels buy us time — reducing diesel dependence now, while we build out longer-term solutions.

So, the real question isn’t if drop-in fuels are needed. It’s how can make them work?

5. The technology levers that I’m following

🌿 Advance the right feedstocks — and the technology behind them

If we want to scale drop-in fuels sustainably, we need to move beyond feedstocks with competing uses like tallow and used cooking oil, as they are in short supply, present price volatility issues, and are in demand across multiple sectors.

Instead, the opportunity lies in developing next-generation feedstocks that are:

Non-edible, high in calorific value, and suited to marginal land (e.g. pongamia, carinata)

Example: Rio Tinto has backed trials of pongamia trees on rehabilitated mine land in Weipa, Queensland — aiming to produce low-carbon biofuel feedstock while restoring biodiversity on degraded sites.

Integrated with domestic agriculture, so we can align cultivation, collection, and logistics with regional supply chains

Crucially, technology can accelerate availability and viability:

Genetic modification and advanced plant breeding are being used to improve oil yield, drought tolerance, and pest resistance — making crops like carinata and pongamia more commercially viable.

Precision agriculture and agronomic modelling are helping identify where these crops can be optimally grown with minimal water and fertiliser inputs.

Bioengineering may also enable tailoring oil properties for better fuel yields or lower processing costs in the future.

By backing technology-enabled, non-food feedstocks, Australia can secure a more scalable, stable, and sovereign supply base for drop-in fuels.

🧬 Unlock scale through technologies that enables 2nd and 3rd gen feedstocks

Second- and third-generation feedstocks (like agri-residues and municipal solid waste) offer volume and circularity — but only if we can process them efficiently. Here’s what’s unlocking their value:

Hydrothermal liquefaction (HTL): Converts wet biomass into biocrude without drying.

Example: Arbios Biotech (Arbios), a joint venture of Canadian Forest Products Ltd. (Canfor) and Licella Holdings Ltd. (Licella) plan to convert sawmill residues, primarily bark, into high value renewable biocrude which can be further processed in refineries to produce low-carbon transportation fuels.

Catalytic pyrolysis: Uses heat and catalysts to upgrade woody and fibrous agri-waste into bio-oil.

Example: Anellotech is commercialising this for wood waste, producing renewable aromatic compounds.

These pathways are how we turn underused waste streams into high-value fuels — and reduce our dependency on narrow, high-cost feedstocks.

📈 Invest in high-yield conversion technologies

To bring down cost per litre, we need to get more fuel from each tonne of biomass. Some examples include:

Catalytic hydroprocessing can reduce oxygen content and improve stability, boosting fuel yield and shelf life.

The common thread? How do we reduce the footprint of feedstock cost!

🔬 Rethink hydrogen use in hydrotreating

Hydrotreating is the gold standard for producing renewable diesel — but green hydrogen is currently expensive and scale-constrained, limiting availability.

Potential alternative approaches are emerging:

Hydrogen donor solvents: Using compounds like methanol or ethanol to donate hydrogen in situ during upgrading.

Catalyst innovations: Solid acid catalysts and emerging pathways aim to reduce hydrogen input by improving reaction efficiency.

🙏 Thanks for reading!

Appreciate you joining me on this journey to unpack diesel displacement in Australia. If this sparked a thought, please drop me a message, I’d love to connect.

🔧 Up next: Retrofitting for impact

Can we rewire what we already have? My next blog dives into the role of retrofitting technologies from dual-fuel systems to diesel-hybrid conversions and their potential to shift the needle without starting from scratch.

Stay tuned — it’s one you won’t want to miss. 🚜⚡